%matplotlib inline

import numpy as np

import matplotlib.pyplot as pltPCA Tutorial 2

ML

![]()

import numpy as np

import plotly.graph_objects as go

from plotly.subplots import make_subplots

from ipywidgets import interact, FloatSlider, VBox, HBox, HTML

def make_cov(s1, s2, rho):

return np.array([[s1**2, rho*s1*s2],

[rho*s1*s2, s2**2]])

def ellipse_from_cov(Sigma, k=2.4477, n=200):

vals, vecs = np.linalg.eigh(Sigma)

axes = np.sqrt(vals) * k

t = np.linspace(0, 2*np.pi, n)

circle = np.vstack([np.cos(t), np.sin(t)])

E = (vecs @ np.diag(axes)) @ circle

return E[0], E[1]

def base_layout():

fig = make_subplots(

rows=1, cols=2, column_widths=[0.62, 0.38],

subplot_titles=("Samples + 95% Ellipse", "Covariance Matrix Σ"),

specs=[[{"type":"scatter"}, {"type":"heatmap"}]]

)

fig.update_layout(

height=460, width=980, template="plotly_white",

margin=dict(l=40, r=30, t=60, b=40),

legend=dict(orientation="h", yanchor="bottom", y=1.02, xanchor="right", x=1.0)

)

fig.update_xaxes(title_text="x₁", row=1, col=1)

fig.update_yaxes(title_text="x₂", row=1, col=1)

return fig

def render(s1=1.0, s2=1.6, rho=0.4, n=800, seed=0):

rho = float(np.clip(rho, -0.98, 0.98))

Sigma = make_cov(s1, s2, rho)

rng = np.random.default_rng(seed)

X = rng.multivariate_normal([0.0, 0.0], Sigma, size=n)

ex, ey = ellipse_from_cov(Sigma)

fig = base_layout()

fig.add_trace(go.Scatter(

x=X[:,0], y=X[:,1], mode="markers",

marker=dict(size=4, opacity=0.35),

name="Samples"

), row=1, col=1)

fig.add_trace(go.Scatter(

x=ex, y=ey, mode="lines",

line=dict(width=3, color="#e45756"),

name="95% ellipse"

), row=1, col=1)

vmax = float(np.max(np.abs(Sigma))) or 1.0

# Heatmap with in-cell text; reverse y to align text with cells

fig.add_trace(

go.Heatmap(

z=Sigma,

x=["x₁","x₂"],

y=["x₁","x₂"],

colorscale="RdBu",

zmin=-vmax, zmax=vmax, zmid=0.0,

colorbar=dict(title="Covariance"),

text=[[f"{Sigma[i,j]:.2f}" for j in range(2)] for i in range(2)],

texttemplate="%{text}",

textfont={"size":14, "color":"black"},

hovertemplate="Cov(%{y}, %{x}) = %{z:.2f}<extra></extra>"

),

row=1, col=2

)

# Critical for heatmap/text alignment

fig.update_yaxes(autorange="reversed", row=1, col=2)

lim = 3*max(s1, s2)

fig.update_xaxes(range=[-lim, lim], row=1, col=1)

fig.update_yaxes(range=[-lim, lim], scaleanchor="x1", scaleratio=1, row=1, col=1)

return fig

# Sliders

s1 = FloatSlider(value=1.0, min=0.3, max=3.0, step=0.1, description='σ₁', readout_format='.1f')

s2 = FloatSlider(value=1.6, min=0.3, max=3.0, step=0.1, description='σ₂', readout_format='.1f')

rho = FloatSlider(value=0.4, min=-0.95, max=0.95, step=0.05, description='ρ', readout_format='.2f')

def update(s1, s2, rho):

render(s1=s1, s2=s2, rho=rho).show()

_ = interact(update, s1=s1, s2=s2, rho=rho)import numpy as np

import plotly.graph_objects as go

from plotly.subplots import make_subplots

from ipywidgets import interact, FloatSlider, IntSlider, Dropdown, VBox, HBox, HTML

def equicorr(d, rho):

C = np.full((d, d), rho)

np.fill_diagonal(C, 1.0)

return C

def make_cov(sigmas, rho):

# PSD guard for equicorrelation: rho >= -1/(d-1)

d = len(sigmas)

rho_min = -1.0 / (d - 1) + 1e-6 if d > 1 else -0.999

rho = float(np.clip(rho, rho_min, 0.98))

S = np.diag(sigmas)

C = equicorr(d, rho)

return S @ C @ S

def ellipse_from_cov2(Sigma2, k=2.4477, n=200):

vals, vecs = np.linalg.eigh(Sigma2)

vals = np.clip(vals, 1e-12, None)

axes = np.sqrt(vals) * k

t = np.linspace(0, 2*np.pi, n)

circle = np.vstack([np.cos(t), np.sin(t)])

E = (vecs @ np.diag(axes)) @ circle

return E[0], E[1]

def base_layout():

fig = make_subplots(

rows=1, cols=2, column_widths=[0.62, 0.38],

subplot_titles=("Samples in selected 2D", "Covariance matrix Sigma"),

specs=[[{"type":"scatter"}, {"type":"heatmap"}]]

)

fig.update_layout(

height=520, width=1040, template="plotly_white",

margin=dict(l=40, r=30, t=60, b=40),

legend=dict(orientation="h", yanchor="bottom", y=1.02, xanchor="right", x=1.0)

)

fig.update_xaxes(title_text="x axis", row=1, col=1)

fig.update_yaxes(title_text="y axis", row=1, col=1)

return fig

def render(d=4, s1=1.0, s2=1.2, s3=1.5, s4=0.8, rho=0.4, proj_x=0, proj_y=1, n=1200, seed=0):

sigmas_all = [s1, s2, s3, s4]

sigmas = np.array(sigmas_all[:d], dtype=float)

Sigma = make_cov(sigmas, rho)

rng = np.random.default_rng(seed)

X = rng.multivariate_normal(np.zeros(d), Sigma, size=n)

# 2D projection indices

i, j = int(proj_x), int(proj_y)

i = np.clip(i, 0, d-1); j = np.clip(j, 0, d-1)

if i == j:

j = (i + 1) % d

X2 = X[:, [i, j]]

Sigma2 = Sigma[[i, j]][:, [i, j]]

ex, ey = ellipse_from_cov2(Sigma2)

fig = base_layout()

# Left: samples and 95 percent ellipse

fig.add_trace(go.Scatter(

x=X2[:, 0], y=X2[:, 1], mode="markers",

marker=dict(size=4, opacity=0.35),

name="samples"

), row=1, col=1)

fig.add_trace(go.Scatter(

x=ex, y=ey, mode="lines",

line=dict(width=3, color="#e45756"),

name="95 percent ellipse"

), row=1, col=1)

# Axis equal

lim = 3.5 * max(sigmas[i], sigmas[j])

fig.update_xaxes(range=[-lim, lim], row=1, col=1)

fig.update_yaxes(range=[-lim, lim], scaleanchor="x1", scaleratio=1, row=1, col=1)

# Right: covariance heatmap with values

vmax = float(np.max(np.abs(Sigma)))

vmax = vmax if vmax > 0 else 1.0

labels = [f"x{k+1}" for k in range(d)]

fig.add_trace(

go.Heatmap(

z=Sigma, x=labels, y=labels,

colorscale="RdBu", zmin=-vmax, zmax=vmax, zmid=0.0,

colorbar=dict(title="Covariance"),

text=[[f"{Sigma[r,c]:.2f}" for c in range(d)] for r in range(d)],

texttemplate="%{text}",

textfont={"size":14, "color":"black"},

hovertemplate="Cov(%{y}, %{x}) = %{z:.3f}<extra></extra>"

),

row=1, col=2

)

fig.update_yaxes(autorange="reversed", row=1, col=2)

# Titles

fig.update_xaxes(title_text=f"x{ i+1 }", row=1, col=1)

fig.update_yaxes(title_text=f"x{ j+1 }", row=1, col=1)

return fig

# Widgets

dim = IntSlider(value=4, min=2, max=4, step=1, description="dims")

s1 = FloatSlider(value=1.0, min=0.3, max=3.0, step=0.1, description="sigma1")

s2 = FloatSlider(value=1.2, min=0.3, max=3.0, step=0.1, description="sigma2")

s3 = FloatSlider(value=1.5, min=0.3, max=3.0, step=0.1, description="sigma3")

s4 = FloatSlider(value=0.8, min=0.3, max=3.0, step=0.1, description="sigma4")

rho = FloatSlider(value=0.4, min=-0.95, max=0.95, step=0.05, description="rho")

proj_x = Dropdown(options=[("x1",0),("x2",1),("x3",2),("x4",3)], value=0, description="x axis")

proj_y = Dropdown(options=[("y1",0),("y2",1),("y3",2),("y4",3)], value=1, description="y axis")

def _update_options(d):

opts = [(f"x{k+1}", k) for k in range(d)]

proj_x.options = opts

proj_y.options = opts

_update_options(dim.value)

def update(d, s1, s2, s3, s4, rho, proj_x, proj_y):

_update_options(d)

fig = render(d=d, s1=s1, s2=s2, s3=s3, s4=s4, rho=rho, proj_x=proj_x, proj_y=proj_y)

fig.show()

ui = VBox([

HTML("<b>Interactive multivariate normal</b> Sigma = S Corr S with equicorrelation"),

HBox([dim, rho]),

HBox([s1, s2, s3, s4]),

HBox([proj_x, proj_y])

])

_ = interact(update, d=dim, s1=s1, s2=s2, s3=s3, s4=s4, rho=rho, proj_x=proj_x, proj_y=proj_y)

uiimport numpy as np

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

np.random.seed(42)

n = 200

mean1 = np.zeros(4)

cov1 = np.full((4,4), 0.8)

np.fill_diagonal(cov1, 1)

group1 = np.random.multivariate_normal(mean1, cov1, n)

mean2 = np.zeros(4)

cov2 = np.full((4,4), 0.8)

np.fill_diagonal(cov2, 1)

group2 = np.random.multivariate_normal(mean2, cov2, n)

data = np.hstack((group1, group2))

df = pd.DataFrame(data, columns=["rooms", "bath", "sqft", "garage",

"schools", "crime", "distance", "income"])

df["rooms"] = 3 + df["rooms"] * 1.2

df["bath"] = 2 + df["bath"] * 0.8

df["sqft"] = 1500 + df["sqft"] * 300

df["garage"] = 1 + df["garage"] * 0.5

df["schools"] = 5 + df["schools"] * 1.5

df["crime"] = 50 - df["crime"] * 10

df["distance"] = 10 + df["distance"] * 2

df["income"] = 60000 + df["income"] * 8000

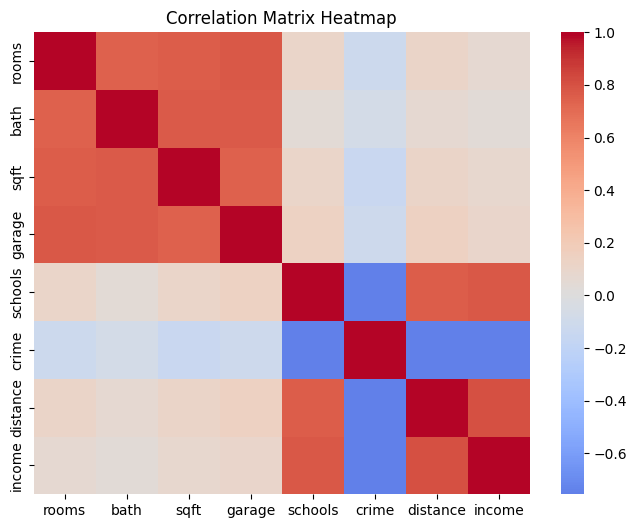

corr = df.corr()

cov = df.cov()

plt.figure(figsize=(8,6))

sns.heatmap(corr, annot=False, cmap='coolwarm', center=0)

plt.title("Correlation Matrix Heatmap")

plt.show()

print("Covariance Matrix:\n", cov)

Covariance Matrix:

rooms bath sqft garage schools \

rooms 1.170565 0.578442 226.712141 0.402969 0.165186

bath 0.578442 0.520655 153.051205 0.265776 0.042117

sqft 226.712141 153.051205 76365.107914 98.431732 41.912809

garage 0.402969 0.265776 98.431732 0.229164 0.096007

schools 0.165186 0.042117 41.912809 0.096007 2.052282

crime -1.244739 -0.508013 -380.886596 -0.521502 -10.258421

distance 0.234267 0.091537 57.394686 0.133176 2.052900

income 590.375758 190.326319 177182.411264 363.295200 8387.138229

crime distance income

rooms -1.244739 0.234267 5.903758e+02

bath -0.508013 0.091537 1.903263e+02

sqft -380.886596 57.394686 1.771824e+05

garage -0.521502 0.133176 3.632952e+02

schools -10.258421 2.052900 8.387138e+03

crime 90.186235 -13.620349 -5.422707e+04

distance -13.620349 3.596559 1.156696e+04

income -54227.067786 11566.961854 5.714393e+07 import numpy as np

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

# Step 1: Your existing dataset

np.random.seed(42)

n = 200

mean1 = np.zeros(4)

cov1 = np.full((4,4), 0.8)

np.fill_diagonal(cov1, 1)

group1 = np.random.multivariate_normal(mean1, cov1, n)

mean2 = np.zeros(4)

cov2 = np.full((4,4), 0.8)

np.fill_diagonal(cov2, 1)

group2 = np.random.multivariate_normal(mean2, cov2, n)

data = np.hstack((group1, group2))

df = pd.DataFrame(data, columns=["rooms", "bath", "sqft", "garage",

"schools", "crime", "distance", "income"])

# Step 2: Apply scaling

df["rooms"] = 3 + df["rooms"] * 1.2

df["bath"] = 2 + df["bath"] * 0.8

df["sqft"] = 1500 + df["sqft"] * 300

df["garage"] = 1 + df["garage"] * 0.5

df["schools"] = 5 + df["schools"] * 1.5

df["crime"] = 50 - df["crime"] * 10

df["distance"] = 10 + df["distance"] * 2

df["income"] = 60000 + df["income"] * 8000

# Step 3: Compute mean and covariance matrix

mean_vec = df.mean().values

cov_mat = df.cov().values

print("Mean vector:\n", np.round(mean_vec, 2))

print("\nCovariance matrix shape:", cov_mat.shape)

# Step 4: Sample new points from same covariance structure

np.random.seed(0)

new_samples = np.random.multivariate_normal(mean_vec, cov_mat, size=500)

# Step 5: Convert to DataFrame

df_new = pd.DataFrame(new_samples, columns=df.columns)

# Step 6: Visualize correlation similarity between original and sampled

fig, axes = plt.subplots(1, 2, figsize=(12, 5))

sns.heatmap(df.corr(), cmap="coolwarm", center=0, ax=axes[0])

axes[0].set_title("Original Correlation")

sns.heatmap(df_new.corr(), cmap="coolwarm", center=0, ax=axes[1])

axes[1].set_title("Sampled Data Correlation")

plt.tight_layout()

plt.show()

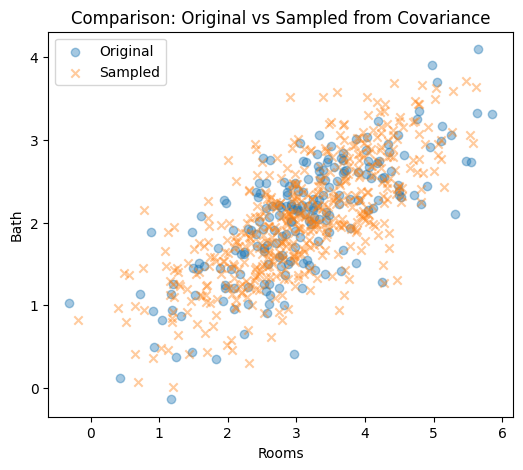

# Step 7: Scatter comparison (check shape similarity)

plt.figure(figsize=(6, 5))

plt.scatter(df["rooms"], df["bath"], alpha=0.4, label="Original")

plt.scatter(df_new["rooms"], df_new["bath"], alpha=0.4, label="Sampled", marker="x")

plt.xlabel("Rooms")

plt.ylabel("Bath")

plt.title("Comparison: Original vs Sampled from Covariance")

plt.legend()

plt.show()Mean vector:

[3.080000e+00 2.050000e+00 1.515330e+03 1.030000e+00 4.840000e+00

5.157000e+01 9.710000e+00 5.931653e+04]

Covariance matrix shape: (8, 8)

data.shape

data=df_newimport numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

# Step 1: Take the sampled dataset

X = df_new.values

n, d = X.shape

print(f"Sampled dataset shape: {n} samples × {d} features")

# Step 2: Center the data

X_centered = X - X.mean(axis=0)

# Step 3: Compute covariance matrix

Sigma = (X_centered.T @ X_centered) / (n - 1)

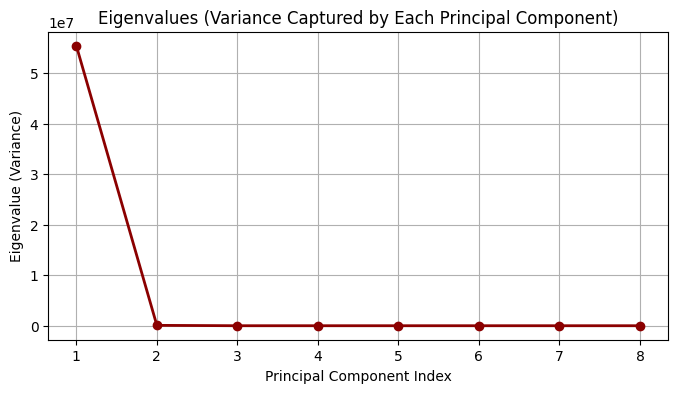

# Step 4: Eigen-decomposition

eigvals, eigvecs = np.linalg.eigh(Sigma)

idx = np.argsort(eigvals)[::-1]

eigvals, eigvecs = eigvals[idx], eigvecs[:, idx]

print("Eigenvalues:\n", np.round(eigvals, 2))

print("\nFirst 3 Eigenvectors (Principal Directions):\n", np.round(eigvecs[:, :3], 3))

# Step 5: Plot eigenvalues (variance explained)

plt.figure(figsize=(8, 4))

plt.plot(range(1, d + 1), eigvals, 'o-', color='darkred', linewidth=2)

plt.title("Eigenvalues (Variance Captured by Each Principal Component)")

plt.xlabel("Principal Component Index")

plt.ylabel("Eigenvalue (Variance)")

plt.grid(True)

plt.show()

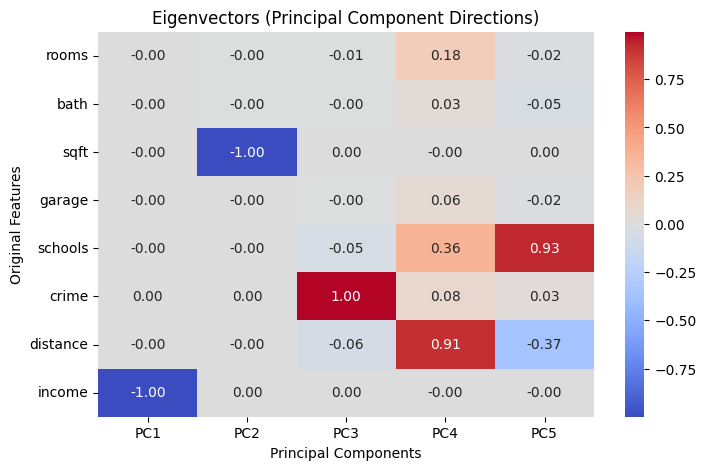

# Step 6: Plot eigenvectors as heatmap

plt.figure(figsize=(8, 5))

sns.heatmap(eigvecs[:, :5],

annot=True, fmt=".2f", cmap="coolwarm",

xticklabels=[f"PC{i+1}" for i in range(5)],

yticklabels=df_new.columns)

plt.title("Eigenvectors (Principal Component Directions)")

plt.xlabel("Principal Components")

plt.ylabel("Original Features")

plt.tight_layoutSampled dataset shape: 500 samples × 8 features

Eigenvalues:

[5.53943018e+07 7.29818700e+04 3.48300000e+01 1.06000000e+00

5.80000000e-01 5.00000000e-01 1.70000000e-01 6.00000000e-02]

First 3 Eigenvectors (Principal Directions):

[[-0. -0.003 -0.009]

[-0. -0.002 -0.002]

[-0.001 -1. 0.002]

[-0. -0.001 -0.004]

[-0. -0. -0.055]

[ 0.001 0.002 0.996]

[-0. -0. -0.063]

[-1. 0.001 0.001]]

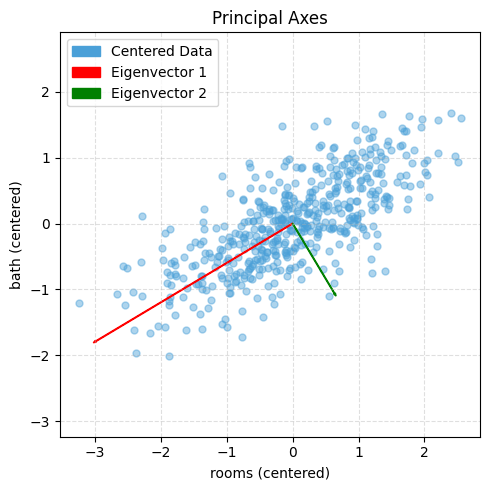

# Plot centered data with principal axes (like the example figure)

import numpy as np

import matplotlib.pyplot as plt

from matplotlib.patches import Patch

# ---- choose any two features; here: rooms vs bath from df_new ----

X2 = df_new[["rooms", "bath"]].values

# Center

M = X2 - X2.mean(axis=0)

# Covariance and eigendecomposition

Sigma = (M.T @ M) / (len(M) - 1)

eigvals, eigvecs = np.linalg.eigh(Sigma)

idx = np.argsort(eigvals)[::-1]

eigvals, eigvecs = eigvals[idx], eigvecs[:, idx]

# Scale arrows by sqrt(variance) for visibility

scale = 3.0

v1 = eigvecs[:, 0] * np.sqrt(eigvals[0]) * scale

v2 = eigvecs[:, 1] * np.sqrt(eigvals[1]) * scale

# Plot

plt.figure(figsize=(5, 5))

plt.scatter(M[:, 0], M[:, 1], s=25, alpha=0.45, color="#4aa0d8", label="Centered Data")

# Eigenvector 1 (red) and 2 (green)

plt.arrow(0, 0, v1[0], v1[1], color="red", width=0.01, length_includes_head=True)

plt.arrow(0, 0, v2[0], v2[1], color="green", width=0.01, length_includes_head=True)

# Legend blocks to match styles

legend_elements = [

Patch(facecolor="#4aa0d8", edgecolor="#4aa0d8", label="Centered Data"),

Patch(facecolor="red", edgecolor="red", label="Eigenvector 1"),

Patch(facecolor="green", edgecolor="green", label="Eigenvector 2"),

]

plt.legend(handles=legend_elements, loc="upper left", frameon=True)

plt.title("Principal Axes")

plt.xlabel("rooms (centered)")

plt.ylabel("bath (centered)")

plt.axis('equal')

plt.grid(True, linestyle="--", alpha=0.4)

plt.tight_layout()

plt.show()

# Choose which centered matrix to use:

M = Xc # variance-based PCA (sensitive to units)

# M = Z # correlation-based PCA (unitless)

# Covariance (d×d)

Sigma = (M.T @ M) / (n - 1) # identical to np.cov(M, rowvar=False)

# Eigen-decomposition

eigvals, eigvecs = np.linalg.eigh(Sigma) # guaranteed symmetric → eigh

# Sort by descending variance

idx = np.argsort(eigvals)[::-1]

eigvals = eigvals[idx] # λ₁ ≥ λ₂ ≥ …

eigvecs = eigvecs[:, idx] # columns = principal axes

# Explained variance

explained_var = eigvals

explained_var_ratio = eigvals / eigvals.sum()

# Scores (project data to PCs): T = M * V

T = M @ eigvecs # shape (n, d)

# Dimensionality reduction to k PCs

k = 2

Vk = eigvecs[:, :k] # (d, k)

Tk = M @ Vk # (n, k)

# Optional reconstruction from k PCs (to see information loss)

M_hat = Tk @ Vk.T # (n, d)

recon_rmse = np.sqrt(np.mean((M - M_hat)**2))

print("Explained variance ratio:", explained_var_ratio)

print("RMSE (k PCs reconstruction):", recon_rmse)Explained variance ratio: [0.43959614 0.41253489 0.02638563 0.02521931 0.02480742 0.02446876

0.0238426 0.02314524]

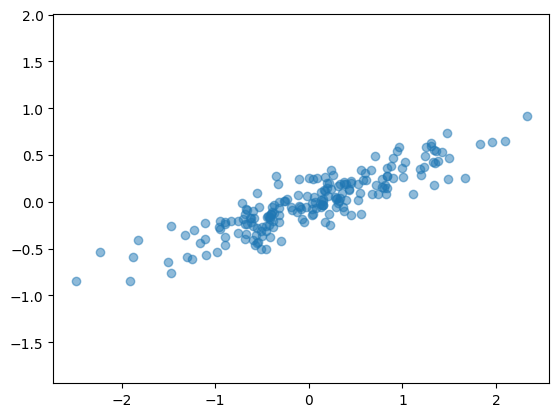

RMSE (k PCs reconstruction): 0.3864285158563806rng = np.random.RandomState(1)

X = np.dot(rng.rand(2, 2), rng.randn(2, 200)).T # shape: (200, 2)

plt.scatter(X[:, 0], X[:, 1], alpha=0.5, label="Original Data")

plt.axis('equal');

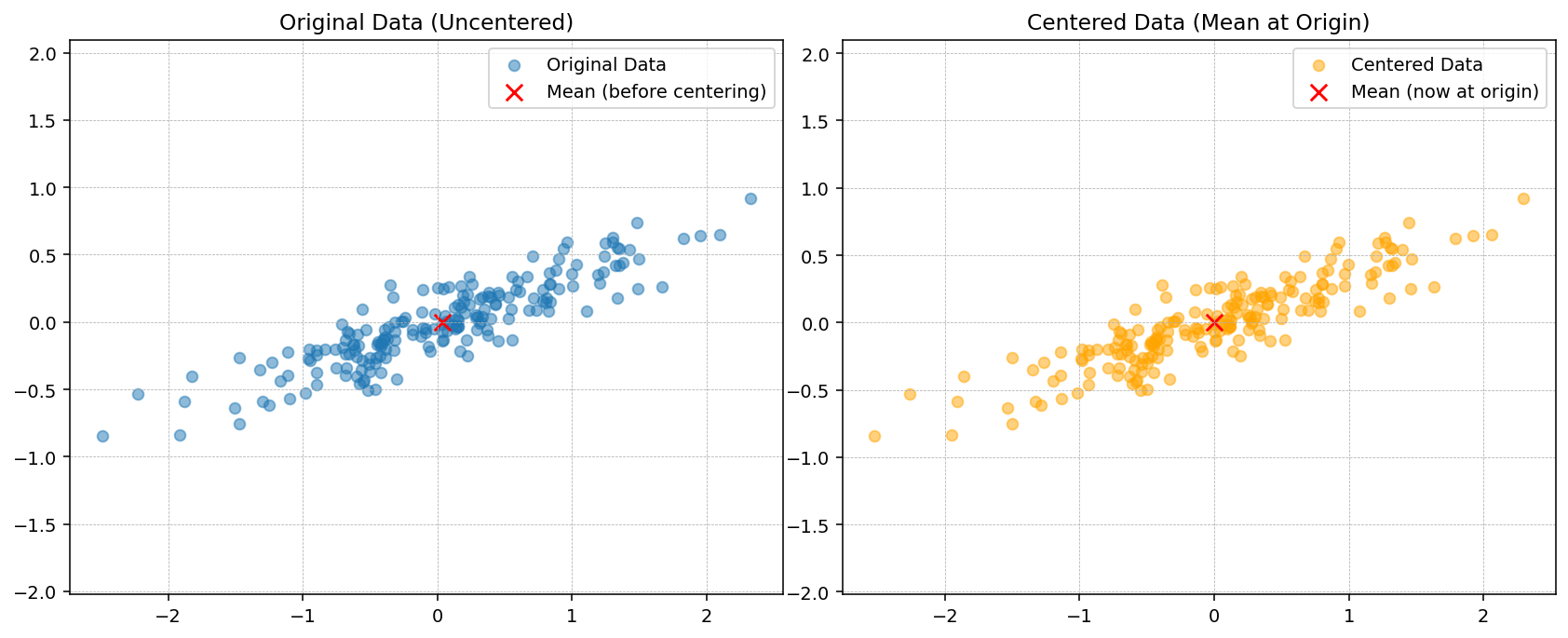

# Step 1: Mean of each feature

mu = X.mean(axis=0)

print("Mean:", mu)

# Step 2: center data

Xc = X - mu

# print("center data",Xc)

plt.figure(figsize=(12, 5), dpi=140)

plt.subplot(1, 2, 1)

plt.scatter(X[:, 0], X[:, 1], alpha=0.5, label="Original Data")

plt.scatter(mu[0], mu[1], color="red", s=80, marker="x", label="Mean (before centering)")

plt.title("Original Data (Uncentered)")

plt.axis("equal")

plt.grid(True, linestyle="--", linewidth=0.4)

plt.legend()

plt.subplot(1, 2, 2)

plt.scatter(Xc[:, 0], Xc[:, 1], alpha=0.5, color="orange", label="Centered Data")

plt.scatter(0, 0, color="red", s=80, marker="x", label="Mean (now at origin)")

plt.title("Centered Data (Mean at Origin)")

plt.axis("equal")

plt.grid(True, linestyle="--", linewidth=0.4)

plt.legend()

plt.tight_layout()

plt.show()Mean: [ 0.03351168 -0.00408072]

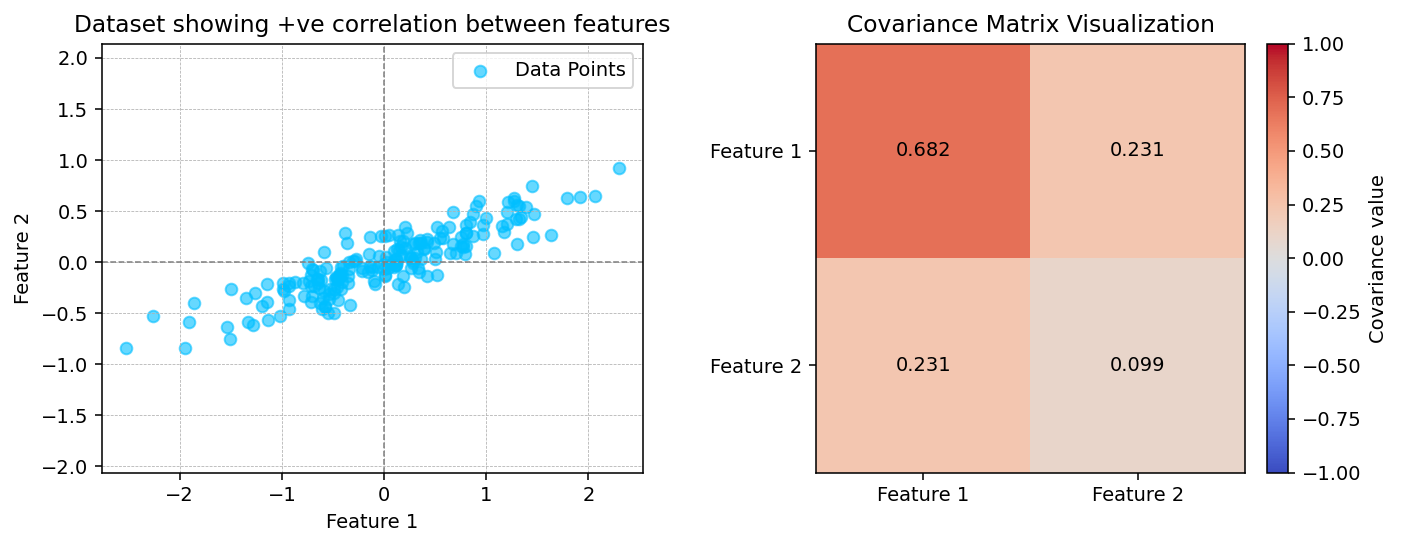

# Step 3: Compute covariance matrix

Sigma = np.cov(Xc.T)

print("Covariance matrix:\n", Sigma)

fig, ax = plt.subplots(1, 2, figsize=(10, 4), dpi=140)

ax[0].scatter(Xc[:, 0], Xc[:, 1], alpha=0.6, color="deepskyblue", label="Data Points")

ax[0].axhline(0, color="gray", linestyle="--", linewidth=0.8)

ax[0].axvline(0, color="gray", linestyle="--", linewidth=0.8)

ax[0].set_title("Dataset showing +ve correlation between features")

ax[0].set_xlabel("Feature 1")

ax[0].set_ylabel("Feature 2")

ax[0].legend()

ax[0].grid(True, linestyle="--", linewidth=0.4)

ax[0].axis("equal")

im = ax[1].imshow(Sigma, cmap="coolwarm", interpolation="nearest", vmin=-1, vmax=1)

plt.colorbar(im, ax=ax[1], fraction=0.046, pad=0.04, label="Covariance value")

ax[1].set_xticks([0, 1])

ax[1].set_yticks([0, 1])

ax[1].set_xticklabels(["Feature 1", "Feature 2"])

ax[1].set_yticklabels(["Feature 1", "Feature 2"])

ax[1].set_title("Covariance Matrix Visualization")

for i in range(2):

for j in range(2):

ax[1].text(j, i, f"{Sigma[i, j]:.3f}",

ha="center", va="center", color="black", fontsize=10)

# plt.suptitle("Covariance Visualization: Dataset with Positive Correlation", fontsize=12)

plt.tight_layout()Covariance matrix:

[[0.68217761 0.23093475]

[0.23093475 0.09883179]]

# # Step 3: Induce negative correlation (invert one feature)

# Xc[:, 1] *= -1 # flip y-axis to make correlation negative

# Sigma = np.cov(Xc.T)

# print("Covariance matrix:\n", Sigma)

# fig, ax = plt.subplots(1, 2, figsize=(10, 4), dpi=140)

# ax[0].scatter(Xc[:, 0], Xc[:, 1], alpha=0.6, color="crimson", label="Data Points")

# ax[0].axhline(0, color="gray", linestyle="--", linewidth=0.8)

# ax[0].axvline(0, color="gray", linestyle="--", linewidth=0.8)

# ax[0].set_title("Dataset showing -ve correlation between features")

# ax[0].set_xlabel("Feature 1 (X₁)")

# ax[0].set_ylabel("Feature 2 (X₂)")

# ax[0].legend()

# ax[0].grid(True, linestyle="--", linewidth=0.4)

# ax[0].axis("equal")

# im = ax[1].imshow(Sigma, cmap="coolwarm", interpolation="nearest", vmin=-1, vmax=1)

# plt.colorbar(im, ax=ax[1], fraction=0.046, pad=0.04, label="Covariance value")

# ax[1].set_xticks([0, 1])

# ax[1].set_yticks([0, 1])

# ax[1].set_xticklabels(["Feature 1", "Feature 2"])

# ax[1].set_yticklabels(["Feature 1", "Feature 2"])

# ax[1].set_title("Covariance Matrix Visualization")

# for i in range(2):

# for j in range(2):

# ax[1].text(j, i, f"{Sigma[i, j]:.3f}",

# ha="center", va="center", color="black", fontsize=10)

# plt.tight_layout()# Step 4: Eigen-decomposition

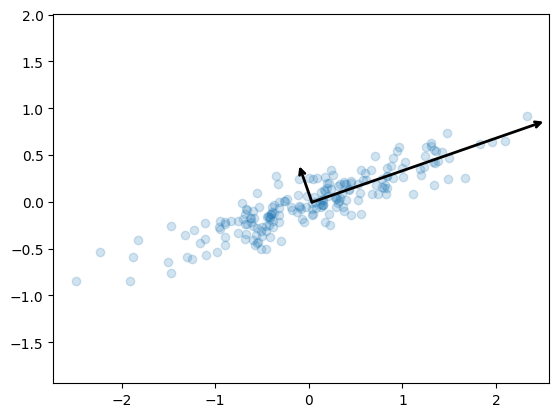

eigvals, eigvecs = np.linalg.eig(Sigma)

print("Eigenvalues:", eigvals)

print("Eigenvectors (columns):\n", eigvecs)

idx = np.argsort(eigvals)[::-1]

eigvals = eigvals[idx]

eigvecs = eigvecs[:, idx]

plt.figure(figsize=(4, 4), dpi=140)

plt.scatter(Xc[:, 0], Xc[:, 1], alpha=0.4, label="Centered Data")

origin = np.array([0, 0])

for i in range(2):

vec = eigvecs[:, i] * np.sqrt(eigvals[i]) * 3

plt.arrow(origin[0], origin[1], vec[0], vec[1],

width=0.02, color="red" if i == 0 else "green",

length_includes_head=True,

label=f"Eigenvector {i+1}")

plt.axis("equal")

plt.title("Principal Axes")

plt.legend()

plt.grid(True, linestyle="--", linewidth=0.4)

plt.show()Eigenvalues: [0.7625315 0.0184779]

Eigenvectors (columns):

[[ 0.94446029 -0.32862557]

[ 0.32862557 0.94446029]]

Using Scikit Learn

from sklearn.decomposition import PCA

# n_components=2 means the algorithm will find two orthogonal axes that capture as much variance as possible.

pca = PCA(n_components=2)

pca.fit(X)PCA(n_components=2)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

PCA(n_components=2)

The fit learns some quantities from the data, most importantly the components and explained variance:

print(pca.components_)[[ 0.94446029 0.32862557]

[-0.32862557 0.94446029]]print(pca.explained_variance_)[0.7625315 0.0184779]def draw_vector(v0, v1, ax=None):

ax = ax or plt.gca()

arrowprops=dict(arrowstyle='->', linewidth=2,

shrinkA=0, shrinkB=0)

ax.annotate('', v1, v0, arrowprops=arrowprops)

# plot data

plt.scatter(X[:, 0], X[:, 1], alpha=0.2)

for length, vector in zip(pca.explained_variance_, pca.components_):

v = vector * 3 * np.sqrt(length)

draw_vector(pca.mean_, pca.mean_ + v)

plt.axis('equal');

- This transformation from data axes to principal axes is an affine transformation, which means it is composed of a translation, rotation, and uniform scaling.

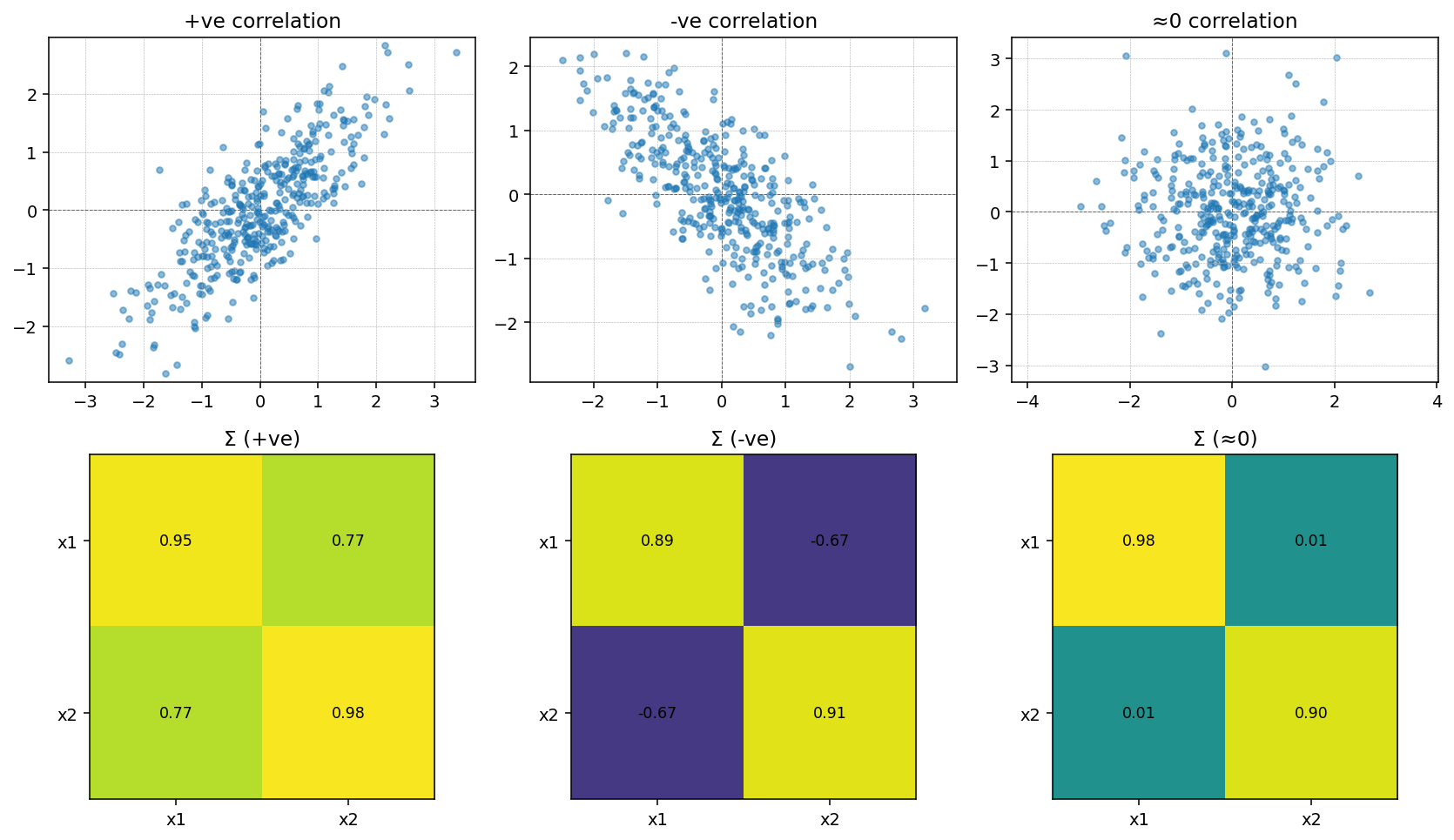

Covariance matrix visualizations (+ve, −ve correlations)

np.random.seed(42)

n = 400

mean = [0, 0]

cov_pos = [[1, 0.8], [0.8, 1]]

cov_neg = [[1, -0.8], [-0.8, 1]]

cov_zero = [[1, 0.0], [0.0, 1]]

X_pos = np.random.multivariate_normal(mean, cov_pos, n)

X_neg = np.random.multivariate_normal(mean, cov_neg, n)

X_zero = np.random.multivariate_normal(mean, cov_zero, n)

datasets = [X_pos, X_neg, X_zero]

titles_scatter = ["+ve correlation", "-ve correlation", "≈0 correlation"]

titles_cov = ["Σ (+ve)", "Σ (-ve)", "Σ (≈0)"]

fig, ax = plt.subplots(2, 3, figsize=(12, 7), dpi=140)

for j, X in enumerate(datasets):

mu = X.mean(axis=0)

Xc = X - mu

Sigma = np.cov(Xc.T)

# scatter

ax[0, j].scatter(Xc[:, 0], Xc[:, 1], alpha=0.5, s=12)

ax[0, j].set_title(titles_scatter[j])

ax[0, j].axhline(0, linestyle="--", linewidth=0.5)

ax[0, j].axvline(0, linestyle="--", linewidth=0.5)

ax[0, j].axis("equal")

ax[0, j].grid(True, linestyle="--", linewidth=0.3)

# covariance heatmap

im = ax[1, j].imshow(Sigma, vmin=-1, vmax=1, interpolation="nearest")

ax[1, j].set_xticks([0, 1]); ax[1, j].set_yticks([0, 1])

ax[1, j].set_xticklabels(["x1", "x2"]); ax[1, j].set_yticklabels(["x1", "x2"])

ax[1, j].set_title(titles_cov[j])

for r in range(2):

for c in range(2):

ax[1, j].text(c, r, f"{Sigma[r, c]:.2f}", ha="center", va="center", fontsize=9)

# fig.colorbar(im, ax=ax[1, :], fraction=0.046, pad=0.04)

plt.tight_layout(); plt.show()

Visualizing Covariance Structure

PCA is built on the covariance matrix, so it helps to see how covariance encodes the relationships between features. Below we construct two toy Gaussian datasets by sampling from a specified covariance matrix: one with a strong positive correlation and one with a strong negative correlation.

Sampling with np.random.multivariate_normal lets us translate a desired covariance structure directly into synthetic data. With positive covariance the samples align with the \(+45^{\circ}\) diagonal, while a negative covariance flips the cloud onto the \(-45^{\circ}\) diagonal. PCA uses these same covariance patterns to decide which axes (principal components) capture the dominant variability.

PCA as Dimensionality Reduction

Using PCA for dimensionality reduction involves zeroing out one or more of the smallest principal components, resulting in a lower-dimensional projection of the data that preserves the maximal data variance.

Here is an example of using PCA as a dimensionality reduction transform:

pca = PCA(n_components=1)

pca.fit(X)

X_pca = pca.transform(X)

print("original shape: ", X.shape)

print("transformed shape:", X_pca.shape)original shape: (200, 2)

transformed shape: (200, 1)The transformed data has been reduced to a single dimension. To understand the effect of this dimensionality reduction, we can perform the inverse transform of this reduced data and plot it along with the original data (see the following figure):

X_new = pca.inverse_transform(X_pca)

plt.scatter(X[:, 0], X[:, 1], alpha=0.2)

plt.scatter(X_new[:, 0], X_new[:, 1], alpha=0.8)

plt.axis('equal');

The light points are the original data, while the dark points are the projected version. This makes clear what a PCA dimensionality reduction means: the information along the least important principal axis or axes is removed, leaving only the component(s) of the data with the highest variance. The fraction of variance that is cut out (proportional to the spread of points about the line formed in the preceding figure) is roughly a measure of how much “information” is discarded in this reduction of dimensionality.

This reduced-dimension dataset is in some senses “good enough” to encode the most important relationships between the points: despite reducing the number of data features by 50%, the overall relationships between the data points are mostly preserved.

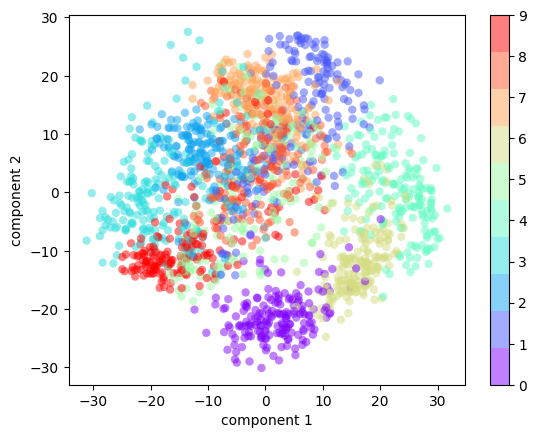

PCA for Visualization: Handwritten Digits

The usefulness of dimensionality reduction may not be entirely apparent in only two dimensions, but it becomes clear when looking at high-dimensional data. To see this, let’s take a quick look at the application of PCA to the digits dataset we worked with in In-Depth: Decision Trees and Random Forests.

We’ll start by loading the data:

from sklearn.datasets import load_digits

digits = load_digits()

digits.data.shape(1797, 64)Recall that the digits dataset consists of 8 × 8–pixel images, meaning that they are 64-dimensional. To gain some intuition into the relationships between these points, we can use PCA to project them into a more manageable number of dimensions, say two:

pca = PCA(2) # project from 64 to 2 dimensions

projected = pca.fit_transform(digits.data)

print(digits.data.shape)

print(projected.shape)(1797, 64)

(1797, 2)We can now plot the first two principal components of each point to learn about the data, as seen in the following figure:

plt.scatter(projected[:, 0], projected[:, 1],

c=digits.target, edgecolor='none', alpha=0.5,

cmap=plt.cm.get_cmap('rainbow', 10))

plt.xlabel('component 1')

plt.ylabel('component 2')

plt.colorbar();

Recall what these components mean: the full data is a 64-dimensional point cloud, and these points are the projection of each data point along the directions with the largest variance. Essentially, we have found the optimal stretch and rotation in 64-dimensional space that allows us to see the layout of the data in two dimensions, and we have done this in an unsupervised manner—that is, without reference to the labels.

What Do the Components Mean?

We can go a bit further here, and begin to ask what the reduced dimensions mean. This meaning can be understood in terms of combinations of basis vectors. For example, each image in the training set is defined by a collection of 64 pixel values, which we will call the vector \(x\):

\[ x = [x_1, x_2, x_3 \cdots x_{64}] \]

One way we can think about this is in terms of a pixel basis. That is, to construct the image, we multiply each element of the vector by the pixel it describes, and then add the results together to build the image:

\[ {\rm image}(x) = x_1 \cdot{\rm (pixel~1)} + x_2 \cdot{\rm (pixel~2)} + x_3 \cdot{\rm (pixel~3)} \cdots x_{64} \cdot{\rm (pixel~64)} \]

One way we might imagine reducing the dimensionality of this data is to zero out all but a few of these basis vectors. For example, if we use only the first eight pixels, we get an eight-dimensional projection of the data (the following figure). However, it is not very reflective of the whole image: we’ve thrown out nearly 90% of the pixels!

The upper row of panels shows the individual pixels, and the lower row shows the cumulative contribution of these pixels to the construction of the image. Using only eight of the pixel-basis components, we can only construct a small portion of the 64-pixel image. Were we to continue this sequence and use all 64 pixels, we would recover the original image.

But the pixel-wise representation is not the only choice of basis. We can also use other basis functions, which each contain some predefined contribution from each pixel, and write something like:

\[ image(x) = {\rm mean} + x_1 \cdot{\rm (basis~1)} + x_2 \cdot{\rm (basis~2)} + x_3 \cdot{\rm (basis~3)} \cdots \]

PCA can be thought of as a process of choosing optimal basis functions, such that adding together just the first few of them is enough to suitably reconstruct the bulk of the elements in the dataset. The principal components, which act as the low-dimensional representation of our data, are simply the coefficients that multiply each of the elements in this series. the following figure shows a similar depiction of reconstructing the same digit using the mean plus the first eight PCA basis functions.

Unlike the pixel basis, the PCA basis allows us to recover the salient features of the input image with just a mean, plus eight components! The amount of each pixel in each component is the corollary of the orientation of the vector in our two-dimensional example. This is the sense in which PCA provides a low-dimensional representation of the data: it discovers a set of basis functions that are more efficient than the native pixel basis of the input data.

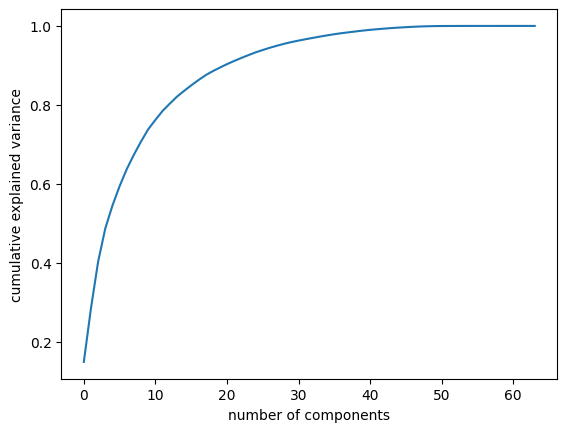

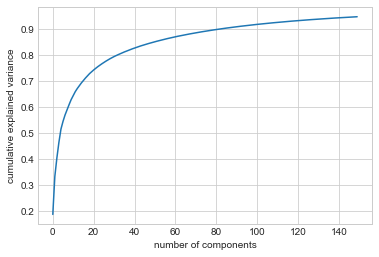

Choosing the Number of Components

A vital part of using PCA in practice is the ability to estimate how many components are needed to describe the data. This can be determined by looking at the cumulative explained variance ratio as a function of the number of components (see the following figure):

pca = PCA().fit(digits.data)

plt.plot(np.cumsum(pca.explained_variance_ratio_))

plt.xlabel('number of components')

plt.ylabel('cumulative explained variance');

This curve quantifies how much of the total, 64-dimensional variance is contained within the first \(N\) components. For example, we see that with the digits data the first 10 components contain approximately 75% of the variance, while you need around 50 components to describe close to 100% of the variance.

This tells us that our 2-dimensional projection loses a lot of information (as measured by the explained variance) and that we’d need about 20 components to retain 90% of the variance. Looking at this plot for a high-dimensional dataset can help you understand the level of redundancy present in its features.

PCA as Noise Filtering

PCA can also be used as a filtering approach for noisy data. The idea is this: any components with variance much larger than the effect of the noise should be relatively unaffected by the noise. So, if you reconstruct the data using just the largest subset of principal components, you should be preferentially keeping the signal and throwing out the noise.

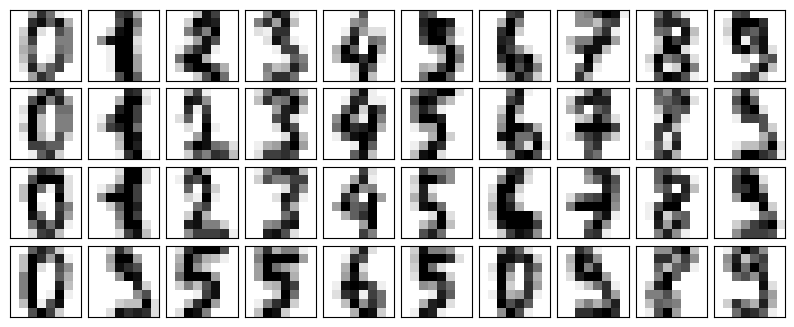

Let’s see how this looks with the digits data. First we will plot several of the input noise-free input samples (the following figure):

def plot_digits(data):

fig, axes = plt.subplots(4, 10, figsize=(10, 4),

subplot_kw={'xticks':[], 'yticks':[]},

gridspec_kw=dict(hspace=0.1, wspace=0.1))

for i, ax in enumerate(axes.flat):

ax.imshow(data[i].reshape(8, 8),

cmap='binary', interpolation='nearest',

clim=(0, 16))

plot_digits(digits.data)

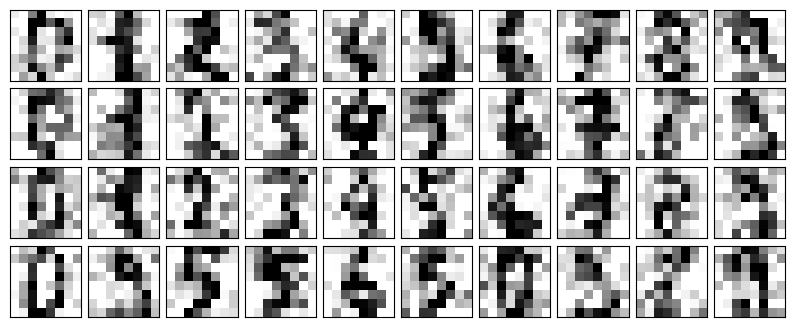

Now let’s add some random noise to create a noisy dataset, and replot it (the following figure):

rng = np.random.default_rng(42)

rng.normal(10, 2)10.609434159508863rng = np.random.default_rng(42)

noisy = rng.normal(digits.data, 4)

plot_digits(noisy)

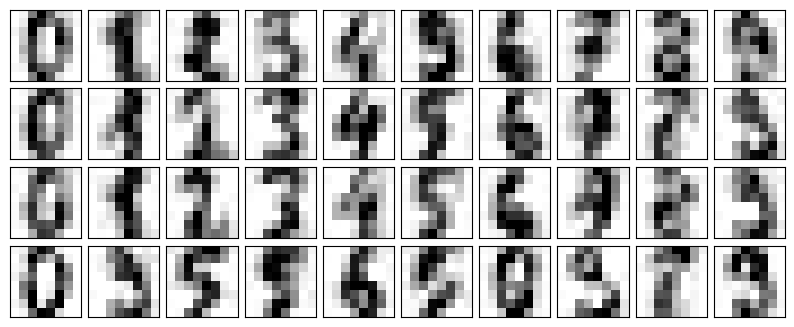

The visualization makes the presence of this random noise clear. Let’s train a PCA model on the noisy data, requesting that the projection preserve 50% of the variance:

pca = PCA(0.50).fit(noisy)

pca.n_components_12Here 50% of the variance amounts to 12 principal components, out of the 64 original features. Now we compute these components, and then use the inverse of the transform to reconstruct the filtered digits; the following figure shows the result:

components = pca.transform(noisy)

filtered = pca.inverse_transform(components)

plot_digits(filtered)

This signal preserving/noise filtering property makes PCA a very useful feature selection routine—for example, rather than training a classifier on very high-dimensional data, you might instead train the classifier on the lower-dimensional principal component representation, which will automatically serve to filter out random noise in the inputs.

PCA and Multicollinearity: Housing Example

Many real-world tabular datasets contain strongly correlated (multicollinear) features, which can make linear models unstable. Here we revisit the California housing dataset to see how PCA re-expresses these features into uncorrelated components.

import numpy as np

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

np.random.seed(42)

n = 200

mean1 = np.zeros(4)

cov1 = np.full((4,4), 0.8)

np.fill_diagonal(cov1, 1)

group1 = np.random.multivariate_normal(mean1, cov1, n)

mean2 = np.zeros(4)

cov2 = np.full((4,4), 0.8)

np.fill_diagonal(cov2, 1)

group2 = np.random.multivariate_normal(mean2, cov2, n)

data = np.hstack((group1, group2))

df = pd.DataFrame(data, columns=["rooms", "bath", "sqft", "garage",

"schools", "crime", "distance", "income"])

df["rooms"] = 3 + df["rooms"] * 1.2

df["bath"] = 2 + df["bath"] * 0.8

df["sqft"] = 1500 + df["sqft"] * 300

df["garage"] = 1 + df["garage"] * 0.5

df["schools"] = 5 + df["schools"] * 1.5

df["crime"] = 50 - df["crime"] * 10

df["distance"] = 10 + df["distance"] * 2

df["income"] = 60000 + df["income"] * 8000

corr = df.corr()

cov = df.cov()

plt.figure(figsize=(8,6))

sns.heatmap(corr, annot=False, cmap='coolwarm', center=0)

plt.title("Correlation Matrix Heatmap")

plt.show()

print("Covariance Matrix:\n", cov)

Covariance Matrix:

rooms bath sqft garage schools \

rooms 1.170565 0.578442 226.712141 0.402969 0.165186

bath 0.578442 0.520655 153.051205 0.265776 0.042117

sqft 226.712141 153.051205 76365.107914 98.431732 41.912809

garage 0.402969 0.265776 98.431732 0.229164 0.096007

schools 0.165186 0.042117 41.912809 0.096007 2.052282

crime -1.244739 -0.508013 -380.886596 -0.521502 -10.258421

distance 0.234267 0.091537 57.394686 0.133176 2.052900

income 590.375758 190.326319 177182.411264 363.295200 8387.138229

crime distance income

rooms -1.244739 0.234267 5.903758e+02

bath -0.508013 0.091537 1.903263e+02

sqft -380.886596 57.394686 1.771824e+05

garage -0.521502 0.133176 3.632952e+02

schools -10.258421 2.052900 8.387138e+03

crime 90.186235 -13.620349 -5.422707e+04

distance -13.620349 3.596559 1.156696e+04

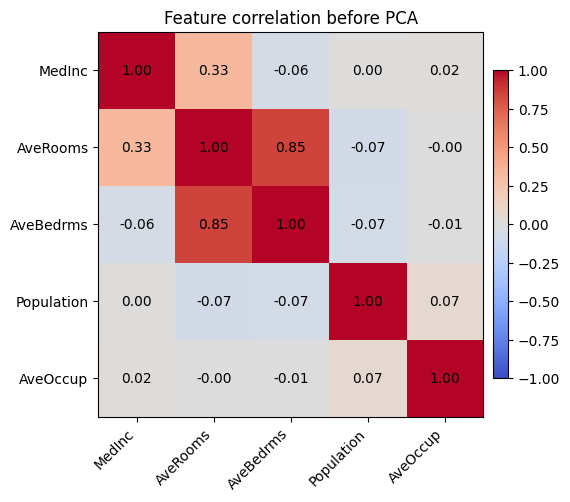

income -54227.067786 11566.961854 5.714393e+07 from sklearn.datasets import fetch_california_housing

from sklearn.preprocessing import StandardScaler

housing = fetch_california_housing()

selected_features = ['MedInc', 'AveRooms', 'AveBedrms', 'Population', 'AveOccup']

feature_indices = [housing.feature_names.index(name) for name in selected_features]

X_housing = housing.data[:, feature_indices]

corr = np.corrcoef(X_housing, rowvar=False)

fig, ax = plt.subplots(figsize=(6, 5))

im = ax.imshow(corr, cmap='coolwarm', vmin=-1, vmax=1)

ax.set_xticks(range(len(selected_features)), labels=selected_features, rotation=45, ha='right')

ax.set_yticks(range(len(selected_features)), labels=selected_features)

ax.set_title('Feature correlation before PCA')

for (i, j), value in np.ndenumerate(corr):

ax.text(j, i, f"{value:.2f}", ha='center', va='center', color='black')

fig.colorbar(im, ax=ax, shrink=0.8, pad=0.02)

plt.show()

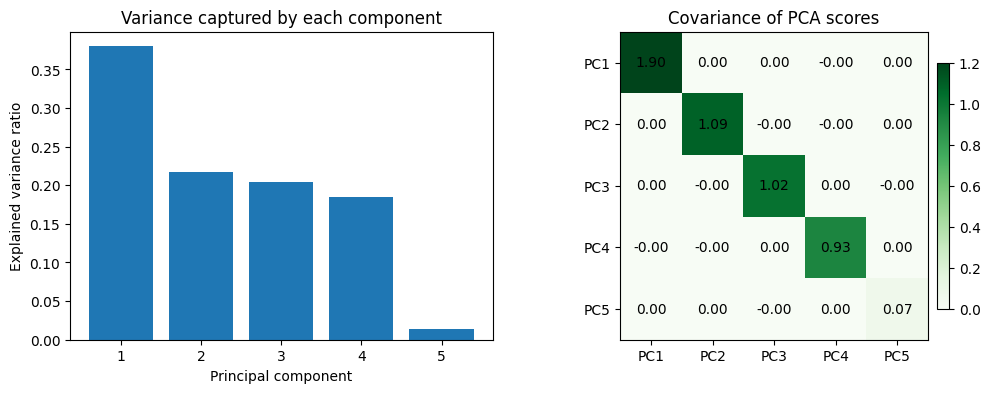

The heatmap highlights that average rooms and average bedrooms are almost the same signal, and occupancy-related features move together as well—exactly the kind of multicollinearity that causes coefficient instability.

scaler = StandardScaler()

X_scaled = scaler.fit_transform(X_housing)

pca_housing = PCA()

housing_components = pca_housing.fit_transform(X_scaled)

component_cov = np.cov(housing_components, rowvar=False)

fig, axes = plt.subplots(1, 2, figsize=(12, 4))

axes[0].bar(range(1, len(selected_features) + 1), pca_housing.explained_variance_ratio_, color='tab:blue')

axes[0].set_xlabel('Principal component')

axes[0].set_ylabel('Explained variance ratio')

axes[0].set_title('Variance captured by each component')

axes[0].set_xticks(range(1, len(selected_features) + 1))

im = axes[1].imshow(component_cov, cmap='Greens', vmin=0, vmax=1.2)

axes[1].set_title('Covariance of PCA scores')

axes[1].set_xticks(range(len(selected_features)), labels=[f'PC{i}' for i in range(1, len(selected_features) + 1)])

axes[1].set_yticks(range(len(selected_features)), labels=[f'PC{i}' for i in range(1, len(selected_features) + 1)])

for (i, j), value in np.ndenumerate(component_cov):

axes[1].text(j, i, f"{value:.2f}", ha='center', va='center', color='black')

fig.colorbar(im, ax=axes[1], shrink=0.8, pad=0.02)

plt.show()

print('Covariance matrix of PCA-transformed features:')

print(np.round(component_cov, 3))

Covariance matrix of PCA-transformed features:

[[ 1.899 0. 0. -0. 0. ]

[ 0. 1.086 -0. -0. 0. ]

[ 0. -0. 1.02 0. -0. ]

[-0. -0. 0. 0.926 0. ]

[ 0. 0. -0. 0. 0.069]]After scaling the features, PCA rotates them into orthogonal directions: the covariance matrix of the principal components is almost diagonal. This decorrelation is what removes multicollinearity—the downstream model now sees independent signals ordered by the variance they explain, and we can keep only the leading components if we want an even smaller, well-conditioned feature set.

Example: Eigenfaces

Earlier we explored an example of using a PCA projection as a feature selector for facial recognition with a support vector machine (see In-Depth: Support Vector Machines). Here we will take a look back and explore a bit more of what went into that. Recall that we were using the Labeled Faces in the Wild (LFW) dataset made available through Scikit-Learn:

from sklearn.datasets import fetch_lfw_people

faces = fetch_lfw_people(min_faces_per_person=60)

print(faces.target_names)

print(faces.images.shape)['Ariel Sharon' 'Colin Powell' 'Donald Rumsfeld' 'George W Bush'

'Gerhard Schroeder' 'Hugo Chavez' 'Junichiro Koizumi' 'Tony Blair']

(1348, 62, 47)Let’s take a look at the principal axes that span this dataset. Because this is a large dataset, we will use the "random" eigensolver in the PCA estimator: it uses a randomized method to approximate the first \(N\) principal components more quickly than the standard approach, at the expense of some accuracy. This trade-off can be useful for high-dimensional data (here, a dimensionality of nearly 3,000). We will take a look at the first 150 components:

pca = PCA(150, svd_solver='randomized', random_state=42)

pca.fit(faces.data)PCA(n_components=150, random_state=42, svd_solver='randomized')In this case, it can be interesting to visualize the images associated with the first several principal components (these components are technically known as eigenvectors, so these types of images are often called eigenfaces; as you can see in the following figure, they are as creepy as they sound):

fig, axes = plt.subplots(3, 8, figsize=(9, 4),

subplot_kw={'xticks':[], 'yticks':[]},

gridspec_kw=dict(hspace=0.1, wspace=0.1))

for i, ax in enumerate(axes.flat):

ax.imshow(pca.components_[i].reshape(62, 47), cmap='bone')

The results are very interesting, and give us insight into how the images vary: for example, the first few eigenfaces (from the top left) seem to be associated with the angle of lighting on the face, and later principal vectors seem to be picking out certain features, such as eyes, noses, and lips. Let’s take a look at the cumulative variance of these components to see how much of the data information the projection is preserving (see the following figure):

plt.plot(np.cumsum(pca.explained_variance_ratio_))

plt.xlabel('number of components')

plt.ylabel('cumulative explained variance');

The 150 components we have chosen account for just over 90% of the variance. That would lead us to believe that using these 150 components, we would recover most of the essential characteristics of the data. To make this more concrete, we can compare the input images with the images reconstructed from these 150 components (see the following figure):

# Compute the components and projected faces

pca = pca.fit(faces.data)

components = pca.transform(faces.data)

projected = pca.inverse_transform(components)# Plot the results

fig, ax = plt.subplots(2, 10, figsize=(10, 2.5),

subplot_kw={'xticks':[], 'yticks':[]},

gridspec_kw=dict(hspace=0.1, wspace=0.1))

for i in range(10):

ax[0, i].imshow(faces.data[i].reshape(62, 47), cmap='binary_r')

ax[1, i].imshow(projected[i].reshape(62, 47), cmap='binary_r')

ax[0, 0].set_ylabel('full-dim\ninput')

ax[1, 0].set_ylabel('150-dim\nreconstruction');

The top row here shows the input images, while the bottom row shows the reconstruction of the images from just 150 of the ~3,000 initial features. This visualization makes clear why the PCA feature selection used in In-Depth: Support Vector Machines was so successful: although it reduces the dimensionality of the data by nearly a factor of 20, the projected images contain enough information that we might, by eye, recognize the individuals in each image. This means our classification algorithm only needs to be trained on 150-dimensional data rather than 3,000-dimensional data, which, depending on the particular algorithm we choose, can lead to much more efficient classification.